BOFIT Weekly Review 14/2025

New round of US tariffs could significantly slow global growth

On April 2, the United States president Donald Trump announced “reciprocal” import tariffs of 10–50 % on 185 countries. The US imposed an additional 34 % tariff on China, which, combined with the 20 % tariff on Chinese goods announced earlier, raised the overall additional tariff rate for China to 54 %. It also eliminated the de minimis duty-free exemption on small packages valued at less than $800 from Hong Kong and China. Other major US trade partners hit with additional tariffs include the EU (20 %), Japan (24 %), Taiwan (32 %), as well as Vietnam (46 %) and South Korea (25 %). New tariffs have yet to be placed on Mexico or Canada as 25 % additional tariffs were earlier imposed on both countries (excluding the 10 % tariff on Canadian energy and potash, as well as no tariff for goods compliant with the Canada-US-Mexico trade agreement rules of origin) are now fully in force. No new tariffs have been imposed on Russia as US-Russia trade has already been reduced to very low levels due to sanctions. Ukraine was slapped with an additional 10 % tariff. The announced tariffs are not added on to existing good-specific tariffs. Tariffs on aluminium, steel, cars and car parts are now 25 %. The basic flat 10 % tariff goes into force on April 5, while additional tariffs above 10 % hit on April 9.

The Trump administration claims that country-specific tariffs have been set at levels that rebalance the bilateral goods trade deficit, going so far as to impose the flat 10 % rate on countries that traditionally run trade deficits with the US. In practice, the tariffs have been derived from a simple “back of the envelope” formula: the country in question’s bilateral trade surplus divided by exports to the US, divided by two. If the country had a trade deficit with the US, or the number resulting from the above formula was less than 10 %, a flat 10 % rate was applied.

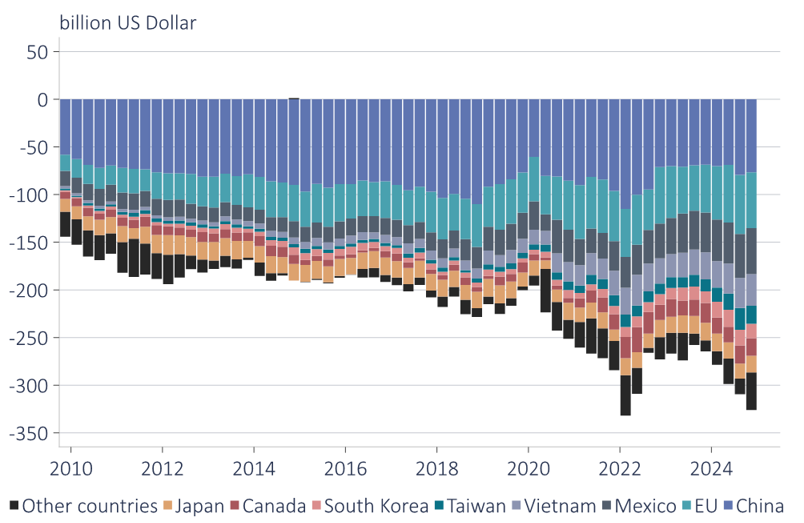

The US last year ran its largest bilateral trade deficit, about $295 billion, with China. Its next largest deficits were with the EU and Mexico. The additional tariffs imposed on China by president Trump in 2018 during his first term initially reduced the bilateral trade deficit, but ultimately failed to lower the US trade deficit with respect to all countries in the world. The situation today is basically a replay of last time around. Although tariffs in principle affect all US trading partners, countries with lower tariffs experience less hurt than countries with higher tariffs. It is expected that high-tariff countries will try to ship their exports to the US via third countries with lower tariff levels either by shifting production to those countries or by performing final assembly or packaging of such goods in those countries. A certain amount of production could also be shifted to the US, but relocation involves taking on higher production costs in the US that reduce the international competitiveness of the relocating firm as well as lower household purchasing power.

Bilateral goods trade deficits of the US with its biggest trading partners

Sources: US Census Bureau and BOFIT.

The imposed tariffs will significantly affect the rates of economic growth in all countries. Researchers at the Kiel Institute for the World Economy calculate that the combined implementation of existing and new tariffs will hurt the US worst of all, with US GDP falling by nearly 2 % compared to the short-term baseline projection. China’s GDP tariffs fell by 0.6 %, the EU 0.3 % and the global economy 1 %. The effects of the tariffs also depend on how other countries respond to US additional tariffs. While specific retaliatory measures are yet unknown, China, the EU and others have said that such responses are under consideration. The scenario calculated by the Bank of Finland in March assumed that the US would institute 25 % tariffs and the EU would respond with retaliatory tariffs of 25 %. Correspondingly, China would be hit with 20 % added tariffs and issue retaliatory tariffs of 20 %. Under this imaginary scenario, the short-term impact would be a decline in US GDP of 0.9 %, the EU -1.0 % and China -1.4 %. The tariff war, however, would bolster uncertainty, thereby hurting fixed investment. As a result, the GDP loss would rise to 1.2 % for the US, 1.5 % for the EU and 2.4 % for China.