BOFIT Forecast for China 2024–2026

2/2024, Published 4 November 2024

The Chinese economy is slowing. Growth in domestic demand has weakened, the downturn in the real estate sector has entered its fourth year and local governments continue to struggle with fiscal problems that restrict government stimulus measures. Thus, even with the stimulus announced in late September, we expect China’s real GDP growth to come in at around 4 percent this year. With cyclical and structural factors constraining growth, real GDP growth should be around 3½ percent next year and close to 3 percent in 2026. Uncertainty surrounding the official economic figures reported by China has increased. China’s growth could exceed our forecast if the government moves quickly on needed economic reforms. In a short-term, a robust fiscal stimulus could fuel growth but given the already very large general government deficit, the stimulus would in medium term increase the pressure to balance general government finances and thus re-straining growth for years to come. The financial sector’s actual condition could also be considerably weaker than reported, darkening the economic outlook.

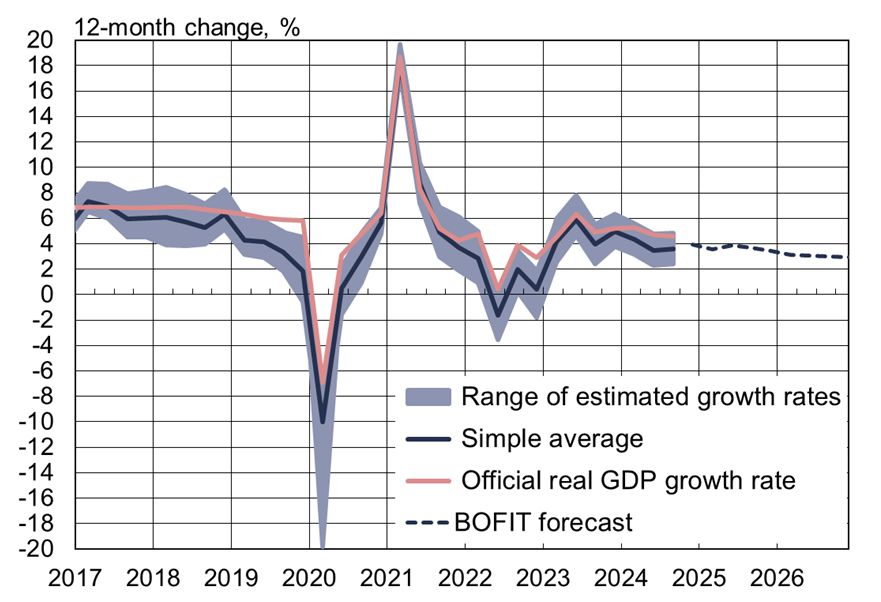

China’s economic growth slowdown has been fairly steady. First-quarter growth was 5.3 % y‑o‑y, second-quarter growth 4.7 %, and third-quarter growth just 4.6 %. BOFIT’s alternative estimate of Chinese GDP also suggest that growth has likely been much lower than the official figures (Fig. 1). To boost growth, the People’s Bank of China (PBoC) adopted a more accommodative monetary stance in late September and hinted further measures could be forthcoming this year. Chinese policymakers also outlined possible fiscal measures to support the growth. Media reports suggest the government plans to issue an additional 3 trillion yuan (about 2 % of GDP) in debt in coming months. While comprehensive information about the planned fiscal policy measures will be released in coming days, the measures should mostly impact growth in next year as the end of this year is already quite near.

With China’s four-decade era of high growth fading, the country is gradually shifting to a growth environment similar to that of developed economies. We expect GDP growth this year to come in at around 4 %. The effects from current stimulus measures becoming evident next year, so we expect GDP growth of around 3½ %. In 2026, growth should slow further to around 3 %, a level close to China’s long-term potential growth rate. The moderated growth pace reflects structural factors such as the shrinking pool of working-age people, an ageing population, sloth-like progress in transitioning China’s investment-driven growth paradigm to a modern consumption-driven economy, inefficient use of resources, an opaque policy environment and weak total productivity trends. Huge branch-specific differences are likely to remain, with certain branches experiencing high growth and others contracting. In any case, 3 % economic growth is still a respectable figure for the world’s largest upper-middle-income nation, and on par with global growth.

Figure 1. BOFIT’s alternative GDP calculation and BOFIT’s forecast for 2024–2026

Sources: China National Bureau of Statistics and BOFIT.

Sources: China National Bureau of Statistics and BOFIT.

NO MAJOR CHANGES IN THE STRUCTURE OF THE ECONOMY

Unlike the other economies of the world, the Chinese economy remains heavily tilted to fixed capital investment (above 40 % of GDP). Despite years of official recognition that the country needs to rebalance its economic structures, no substantial measures have been implemented. Indeed, the structural distortions of overinvestment have been highlighted in recent years as China’s once-booming construction sector enters its fourth consecutive year of contraction. Investment projects involving transportation infrastructure or green transition projects have helped to sustain fixed investment growth, while household consumption, especially in services, has been neglected as a potential economic anchor. Real growth in retail sales has fallen below 2 % this year, and household confidence in the economy is at rock bottom. Factors affecting consumer confidence include weak labour market conditions, the persisting trauma of covid lockdowns and restrictions, the operational challenges facing privately-owned firms and the ongoing erosion of freedom of expression. With two years of failing official efforts to stem sliding real estate market, the incessant drain on household wealth from falling real estate prices is now clearly reflected in consumption demand. Youth unemployment remains extremely high. Media reporting claims that some employers have even gone beyond reducing annual bonuses and other workplace benefits to cutting wages. Although the 50-basis-point cut in interest rates on existing housing loans announced by the PBoC in September should slightly boost disposable household incomes next year, a similar rate cut announced last autumn and implemented in the first half of this year has had only modest impact on consumer behaviour.

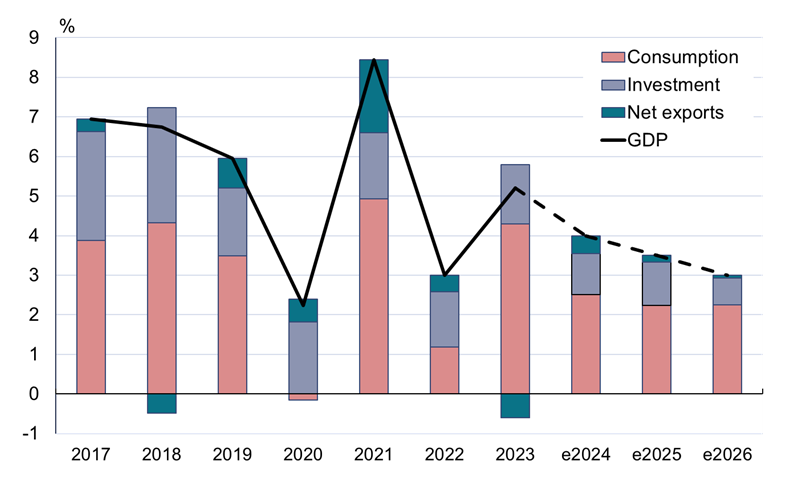

Figure 2. China’s GDP growth, factors contributing to growth and BOFIT Forecast for 2024–2026

Sources: China National Bureau of Statistics, CEIC and BOFIT.

Fixed investment growth has been relatively strong given the ongoing sharp contraction in the real estate sector. Investment has been boosted by government support measures aimed at specific firms in select branches. China’s hands-on industrial policies are expected to continue throughout the forecast period as the country seeks to reduce its dependence on foreign technology and focus on advancing capabilities in strategic branches. The government has pushed ahead aggressively with green transition investments in renewable energy such as wind and solar. After nearly two years of minor measures to halt the real estate sector’s collapse, the government finally seems to be rolling out more serious measures. While more details of the measures will be released in coming days, the measures are likely to be insufficient to dispel depreciation pressure on housing prices over the short term. However, housing construction is expected to plateau in coming years and is unlikely to support growth in the forecast period.

The robust growth in goods exports this year is a bright spot for China’s economy. As at the same time import growth has remained sluggish due to weak household demand, the contribution of net exports to GDP growth has been substantial. Major capital investments in industry during the forecast period should sustain growth in goods exports at levels higher than we earlier forecasted. Moreover, investment in production can reduce import demand to some degree. Even if Chinese products increasingly encounter trade barriers such as Western tariffs and we expect this trend to continue throughout the forecast period, the measures might have little effect to Chinese exports. Studies suggests that Chinese products are increasingly flowing to Western markets via third countries and despite bilateral trade restrictions and deteriorating international relations Chinese value-added is increasingly consumed in the US and Europe. While exports remain strong, the slowdown in domestic economic growth should keep import growth modest. Net exports are expected to support economic growth throughout the entire forecast period.

WEAK PROVINCIAL FINANCES MAKE FISCAL STIMULUS HARDER, WHILE MONETARY ROOM TO MANOEUVRE HAS IMPROVED

China’s sub-national levels of government (provincial, municipal, special administrative regions), which are traditionally responsible for economic stimulus measures, face weak financial situation at the moment. Pre-pandemic local government deficits were already massive, partly due to pursuit of overly ambitious economic targets. Local governments, which bore most of the pandemic costs, must now deal with a collapse in sales of land-use rights, a major source of revenue. Tax cuts and other benefits to companies as a part of state industrial policy, have also had impact on local government revenue streams. International Monetary Fund (IMF) estimates of China’s augmented deficit, which expands the perimeter of government to include government-guided funds and activities of local government financing vehicles (LGFVs), have exceeded 10 % of GDP for over a decade. Unsurprisingly, China’s total government debt currently exceeds 120 % of GDP.

The weakness of provincial finances makes implementation of impactful stimulus measures difficult. While the central government is increasing its deficit by issuing more debt, at the same time provinces face pressure to reduce their spending. To patch their finances, some local governments have resorted to selling off assets. Local governments must also figure out how to pay for the demographic tidal wave of an ageing population as they carry the cost burden of providing healthcare and eldercare. In earlier large-scale economic stimulus programmes, local government financing vehicles played a major role in procuring financing for local government projects while keeping debt off the books. In recent years these offbudget activities have become under more scrutiny, some of the debt has been converted to on-budget debt with lower interest rate. This summer despite the weak economic situation, the finance ministry ordered local governments to refrain from using LGTVs to raise funds for government projects. Moreover, widely publicised arrests and convictions of local decisionmakers in recent years have diminished the risk-taking urges of many local officials. With local governments struggling financially, it falls to the central government to contribute a much larger share of fiscal stimulus funding than earlier. On the whole the current fiscal policy framework is in need of renovation. Under the current revenue model, the central government and local governments collect similar revenue amounts, but local governments are charged with responsibility for most spending. Even if the central government transfers revenue to local governments, they have little ability to adjust their budget revenues. Public finances are not entirely hopeless, however, as there is still strong demand for government bonds. The PBoC even worries that the demand has been too strong driving the interest rates on public debt to be too low. Domestic banks, usually publicly owned, are the biggest buyers of most government debt issues.

The PBoC this summer began regular trading in government treasuries. It emphasised that the actions taken are not similar to quantitative easing done by western central banks in zero-interest-rate environment. On the other hand, it is straightforward to move from the current trading of government bonds to quantitative easing if it is needed. It might become useful monetary policy tool in coming years, as inflation remains stubbornly low. Core inflation (consumer price inflation excluding prices of food and energy) has fallen close to zero. Monetary policy has been eased to boost growth and inflation, with the PBoC signalling further measures are possible before the end of this year. The recent strengthening of the yuan against the dollar has made accommodative monetary policies easier to implement. Markets expect the US Federal Reserve to further lower rates, giving the PBoC more room to ease as the interest-rate difference between them is not expected to widen. Changes in the interest-rate difference are reflected in capital flows, which in turn affect currency exchange rates. The risks from domestic indebtedness, however, are elevated, which could make the central bank cautious on its policy adjustments.

POSITIVE REFORM VIBES

Economic reforms gained momentum this summer. After several decades of hand-wringing, the government announced it was raising the retirement age. From the start of next year, retirement ages will rise incrementally each year so that in 2040 the old-age pension eligibility for men will be 63 years (currently 60 years) and 58 (now 55) for women in office jobs or 55 (now 50) for women in blue-collar jobs. The higher retirement age has long been anticipated in light of longer Chinese life expectancies and long-standing awareness of the economic stress that may result from a shrinking labour force and rapid ageing population. While raising the retirement age helps China’s long-term economic growth prospects, the long transition period and modest increases in the retirement age are unlikely to do much to boost annual rates of economic growth.

The Communist Party’s third plenary session in July laid out several other important reforms. Although details on reform implementation have yet to be released, the reform policies signal a positive change in the party’s focus on long-term growth. One of the more notable objectives is to reduce barriers to internal migration, particularly the movement of people from the countryside to cities. For example, eligibility for public services today usually requires the applicant to show proof of household registration (hukou) in the jurisdiction providing the services. Future applicants for public service position could be registered anywhere in the country and not subject to local hukou requirements. Another proposal would give rural residents the possibility of selling or renting out their rural properties, activities that are currently highly restricted. Traditional rules generally have made it difficult for people to move to cities from the countryside. As to monetary policy changes, central bank governor Pan Gongsheng noted the need for greater transparency and predictability, as well as clarification of the monetary policy framework. Reform of the fiscal policy framework is also under consideration. Although there has been more discussion on reforms boosting long-term economic performance, the emphasis of economic policy remains on developing domestic industries and increasing China’s self-sufficiency. This emphasis might put other needed reforms on the back burner.

UNCERTAINTIES ABOUND

China’s bank-centred financial sector must cope with the effects of the country’s rapid slide into indebtedness in the 2010s, the covid pandemic and the collapse of the real estate sector. Even before the pandemic, the government needed to rescue handful of distressed small and mid-sized banks. Three years of real estate sector decline and the massive pandemic-era impacts on large swathes of the economy such as services have likely degraded the quality of bank lending portfolios. The possibility to postpone loan payments offered to some firms during the height of the pandemic has been extended, with real estate developers now promised that the benefit will run at least until the end of 2026. Some of the troubled LGFVs are also seeking loan extensions for as long as 20 years and seem to face more difficulties to collect their receivables. The slowing economy could also expose hidden problems. For example, fixed investments that showed profit in a high-growth environment, could prove unprofitable in a low-growth environment. A large chunk of bank earnings derive from the interest margin (the difference between lending and deposit rates). The condition of commercial banks has been damaged by the constant erosion of net interest margins. At the end of June, the average net interest margin of banks had fallen to just 1.5 %, down from over 2 % in 2019. China’s big banks are generally considered to be in better shape than small or mid-sized banks. The government’s concerns about the banking sector were reflected this autumn with the government’s announcement of a major cash infusion to China’s six largest banks (1 trillion yuan according to media reports). A crisis in banking sector would both depress growth and require huge public spending to bring the situation back under control.

China’s external relations are expected to remain strained throughout the forecast period. A serious deterioration in foreign relations would at minimum temporarily add to the uncertainty facing firms operating in China or trading with Chinese firms. A slackening of the foreign trade outlook and a broader exit of foreign firms from China would also hurt the growth outlook.

China could experience higher-than-expected growth. For example, the government could introduce more robust stimulus measures than currently contemplated. Aggressive stimulus would increase economic activity over the short run, but in medium term it would increase the pressure to balance general government finances and thus restraining growth for years to come. To improve medium-term growth prospects, China needs to implement market-based reforms that address current structural issues and eliminate barriers. The third plenary session’s proposals for eliminating barriers to internal migration could bring new vibrance and economic growth to urban areas.

Uncertainty pervades Chinese economic statistics. For Chinese bureaucrats tasked with drafting economic policy, dimensioning of measured responses is difficult and vulnerable to errors. The likelihood of major policy mistakes also increases with concentration of power in the hands of a single person. Below-target growth performance typically increases statistical uncertainty as officials are under pressure to produce growth numbers in line with set policy targets. As a result, alternative estimates of Chinese growth might deviate even further from official statistics.