BOFIT Weekly Review 35/2024

Sanctions push CBR to adjust its ruble exchange rate policy

The Central Bank of Russia abandoned its nominal exchange rate target and allowed the ruble to float freely in November 2014. The ruble’s official exchange rate against major currencies used in foreign trade was thereafter based on trading on the Moscow exchange’s foreign currency exchange. (MOEX FX). Although the central bank has sought to moderate swings in the ruble’s external value with such measures as the timing of forex purchases mandated under the government’s fiscal rule, the ruble essentially floated freely up until 2022.

Since the full-scale invasion of Ukraine in February 2022 and the resulting tightening of Western sanctions, the CBR has intervened aggressively in the ruble’s exchange rate with measures that include restrictions on taking forex out of the country and imposing forex repatriation requirements on export firms. The restrictions caused a collapse in the volume of trading on the forex market and a general understanding that the ruble is no longer a freely convertible currency. Ruble trading has also evaporated outside Russia. The European Central Bank, for example, has not posted a ruble-euro reference rate since March 1, 2022.

As of end-June this year, the official ruble-euro and ruble-dollar rates were based on realised trades on the MOEX. With a new round of US sanctions on June 12, 2024, the Moscow exchange suspended all trading in deliverable dollar- and euro-based instruments. With forex trading in dollars and euros basically impossible, trading in Western currencies shifted away from the exchange, causing overall exchange trading to drop by roughly 40 % y-o-y. The ruble’s official rate is now determined exclusively by over-the-counter (OTC) trading. The CBR gathers information from commercial banks on realised trades, which it then uses to set its official daily RUB-USD and RUB-EUR rates.

The OTC market involves direct trading between buyers and sellers. Parties to OTC currency trading in Moscow are typically large export firms or domestic and foreign commercial banks operating within the limits permitted by sanctions. Trading outside the exchange, while flexible and fast, does not generate continuously updated, transparent price information. In the case of the Russian market, this may lead to increased spreads in buy and sell rates. Monitoring of the market is further complicated by the fact that the central bank has ceased to publish statistical data on the OTC forex market.

Bigger role for the Chinese yuan

Trading in other currencies on the Moscow exchange continues uninterrupted. As a result, the ruble-yuan rate has become the most important rate on the Moscow currency exchange. At the start of 2022, there was virtually no yuan demand in Moscow forex trading. The situation changed dramatically after the invasion of Ukraine. In May 2024, yuan-ruble pairings represented slightly over half of all trading on the forex exchange. The growth reflect shifts in the operating space available to the CBR, foreign trade and the banking sector due to sanctions. For some Russian entities, the yuan is the best (and often the only) alternative to the major reserve currencies used in the West.

The yuan is not a fully convertible currency. Only a limited range of yuan-denominated financial instrument exist in Russia, which has led to intermittent shortages that have driven the yuan overnight deposit rate (RUSFAR CNY) briefly above 20 %. The corresponding rate for ruble credit closely tracks the CBR’s key rate, which has stood at 18 % since late July.

The ruble’s nominal exchange rate strengthened slightly in the first half of this year, and the real effective exchange rate reflecting the differences in inflation rates in Russia’s main trading partners was 10 % higher in July than at the start of the year. The dollar’s exchange rate in particular has weakened significantly in recent weeks. A modest drop in the dollar benefits most Russian exporters and increases tax revenues to the state coffers as a large share of Russian export goods are priced in dollars. On the flip side, ruble depreciation makes imported goods more expensive.

Russian imports are further limited by Western sanctions on international payment transmission. The sanctions on Russian financial markets in particular have complicated payment traffic of Russian foreign trade. According to media reports, many Chinese banks have become very cautious about conducting any financial transactions with Russian customers, a situation that explains some of the decline in Chinese exports to Russia in recent months. As a consequence of sanctions, the yuan and ruble have gained increasing use as invoicing currencies in Russian foreign trade. The CBR reports that in June this year about 43 % of imports were invoiced in rubles, 21 % in Western currencies and 36 % in “other currencies” (mostly yuan). However, enabling the sale of products subject to sanctions or entities subject to sanctions can result in significant penalties for third-country financial institutions irrespective of the invoicing currency used. Some Russian foreign trade payments have shifted to cryptocurrencies to evade the traditional banking sector altogether. Complicated payment arrangements add to the price of imported products.

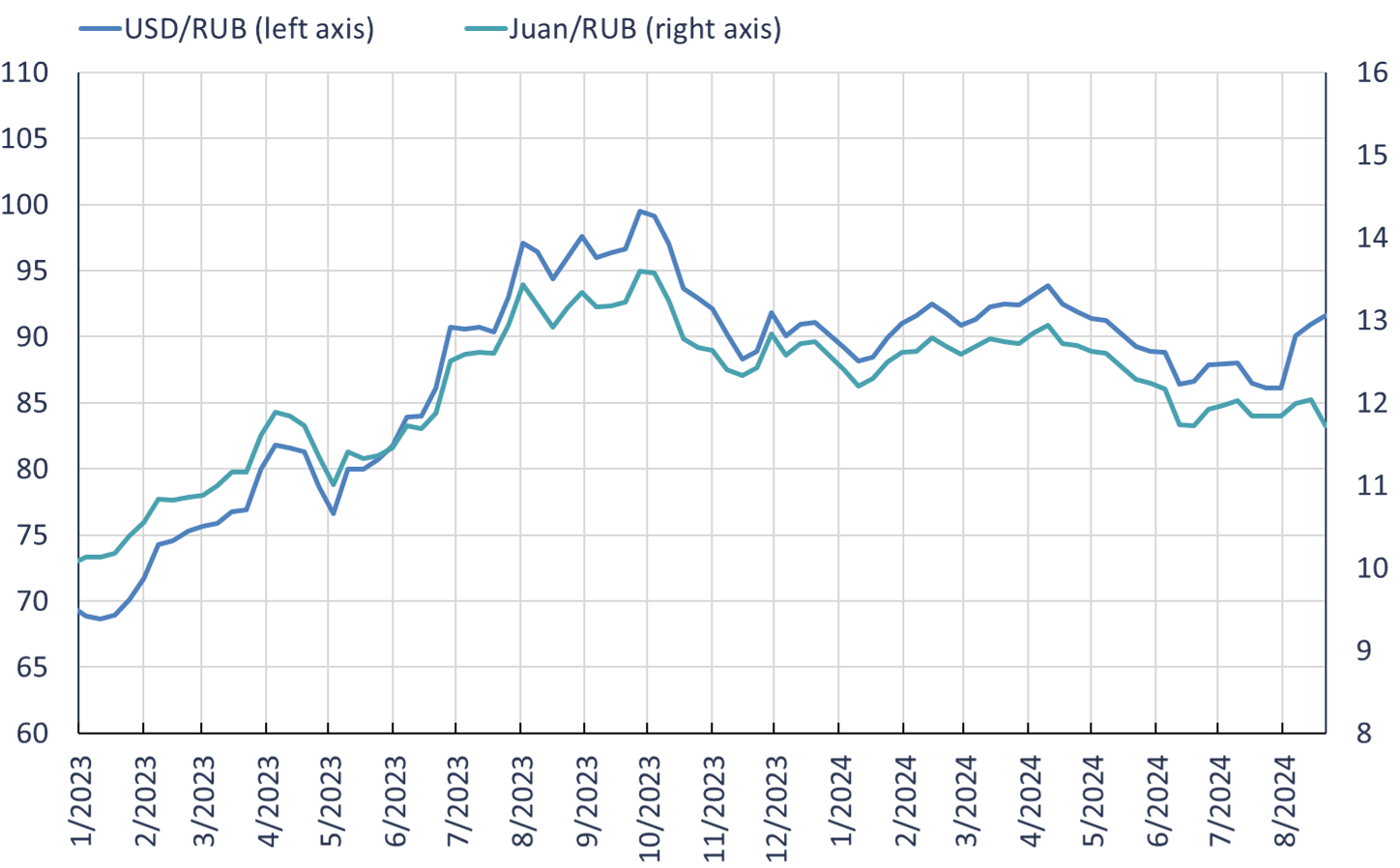

The dollar’s exchange rate has bounced around 85–95 rubles this year, while the yuan rate has dropped to a range of 12–13 rubles

Sources: Central Bank of Russia, CEIC.